Want to Retire Rich? Avoid These 10 States, Study Says

Written by

Joel Anderson

Written by

Joel Anderson

Edited by

Charlotte McMullen

Edited by

Charlotte McMullen

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

You might retire with enough money saved, but that doesn’t necessarily mean it’ll stay that way. In fact, if you pick the wrong place to call home during your golden years, you might run out of retirement savings faster than you anticipated. That’s why a recent GOBankingRates study identified the best states to retire rich if you want to keep more of your money.

Keep reading to see which states offer you the best chance of stretching your retirement savings — and which ones don’t.

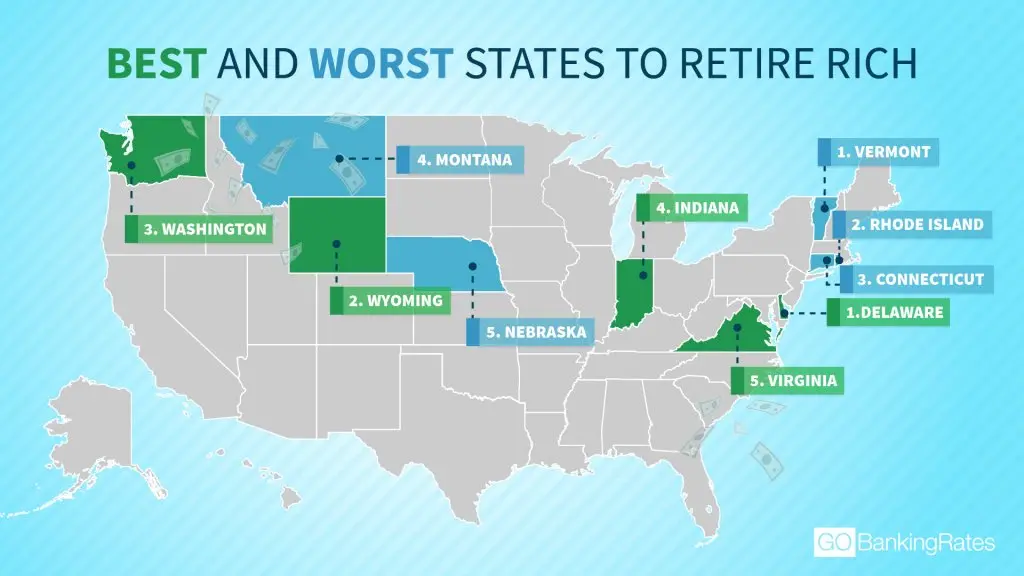

New England Not Great for Retiring Rich

The GOBankingRates study looked at 10 data points across four categories: taxes, living expenses, banking, and healthcare and Social Security. Each factor was scored and weighted to produce a final ranking of the best and worst states if you want to retire rich.

Here’s a look at the 10 worst states:

- Vermont

- Rhode Island

- Connecticut

- Montana

- Nebraska

- Alaska

- New Mexico

- Maine

- North Dakota

- New Jersey

A quick study of these 10 states would immediately reveal that there might be more reasons to avoid making New England your long-term home aside from the cold winters. The top three worst states — Vermont, Rhode Island and Connecticut — are in New England. Another New England state — Maine — also made the top 10, indicating that the region appears to have a collection of factors that make it less inviting for retirees.

There are some bright spots in the New England region, however. For example, New Hampshire ranks as the 10th-best state to retire rich in despite the fact that its property tax rates are the third-highest in the country. New Hampshire is one of just five states with no sales tax, though, which helped boost its final ranking.

Interest Rates Could Be Important

Another trend from the study is the correlation between savings account interest rates and the final rankings. Six of the 10 worst savings account rates are among the bottom 10 states, with Rhode Island, North Dakota, New Mexico, Alaska, Montana and Vermont all offering low returns on their best savings accounts.

When you’re growing your savings in retirement, don’t overlook interest rates. The savings accounts with the higher rates could help you maintain a healthy savings cushion throughout your golden years. However, a recent survey found that 37 percent of consumers never monitor interest rates on their savings products.

Click to See: Arizona vs. Florida — Which State Is Best for Retirees?

How Every State Stacks Up for Rich Retirees

Here’s a look at the full rankings of the best and worst states to retire rich, including some of the scored metrics:

| The Best and Worst States to Retire Rich |

||||||

| Ranking | State | State Sales Tax | Property Tax | Median Home Value | Cost of Living Index | Average Social Security Benefits |

| 1 | Delaware | 0.00% | 0.57% | $268,300 | 102.9 | $1,545.48 |

| 2 | Wyoming | 4.00% | 0.52% | $202,700 | 95.6 | $1,462.92 |

| 3 | Washington | 6.50% | 0.89% | $360,500 | 107.1 | $1,510.94 |

| 4 | Indiana | 7.00% | 0.84% | $126,500 | 91.1 | $1,461.63 |

| 5 | Virginia | 5.30% | 0.84% | $237,900 | 102.2 | $1,494.86 |

| 6 | Maryland | 6.00% | 1.00% | $285,700 | 128.7 | $1,556.20 |

| 7 | Alabama | 4.00% | 0.38% | $128,400 | 90.3 | $1,368.05 |

| 8 | Michigan | 6.00% | 1.39% | $136,600 | 89.7 | $1,485.33 |

| 9 | South Carolina | 6.00% | 0.54% | $150,700 | 99.5 | $1,402.58 |

| 10 | New Hampshire | 0.00% | 1.94% | $271,000 | 115 | $1,567.48 |

| 11 | Arizona | 5.60% | 0.66% | $245,200 | 95.6 | $1,419.88 |

| 12 | Georgia | 4.00% | 0.89% | $163,000 | 90.8 | $1,367.17 |

| 13 | Oregon | 0.00% | 0.95% | $328,600 | 129.3 | $1,419.91 |

| 14 | Louisiana | 5.00% | 0.50% | $140,200 | 94.4 | $1,292.99 |

| 15 | Tennessee | 7.00% | 0.71% | $146,900 | 89.8 | $1,379.71 |

| 16 | Colorado | 2.90% | 0.54% | $366,200 | 102.3 | $1,453.20 |

| 17 | Iowa | 6.00% | 1.45% | $133,500 | 91.3 | $1,439.19 |

| 18 | Arkansas | 6.50% | 0.62% | $123,200 | 87.8 | $1,315.55 |

| 19 | Massachusetts | 6.25% | 1.13% | $395,600 | 132.9 | $1,506.47 |

| 20 | Kentucky | 6.00% | 0.79% | $139,900 | 93.7 | $1,322.96 |

| 21 | Utah | 5.95% | 0.62% | $275,800 | 95.7 | $1,468.16 |

| 22 | Oklahoma | 4.50% | 0.85% | $117,500 | 89.2 | $1,368.77 |

| 23 | North Carolina | 4.75% | 0.83% | $169,000 | 94.6 | $1,401.31 |

| 24 | Idaho | 6.00% | 0.74% | $201,800 | 92.2 | $1,360.87 |

| 25 | Pennsylvania | 6.00% | 1.48% | $168,200 | 102 | $1,478.88 |

| 26 | Mississippi | 7.00% | 0.61% | $120,300 | 85.1 | $1,286.25 |

| 27 | Nevada | 6.85% | 0.65% | $284,000 | 104.7 | $1,333.54 |

| 28 | Florida | 6.00% | 0.90% | $235,400 | 99.3 | $1,359.47 |

| 29 | Wisconsin | 5.00% | 1.67% | $171,400 | 96.2 | $1,471.82 |

| 30 | Hawaii | 4.00% | 0.29% | $749,200 | 188.3 | $1,412.54 |

| 31 | Ohio | 5.75% | 1.55% | $132,400 | 92.3 | $1,369.03 |

| 32 | California | 7.25% | 0.71% | $543,100 | 141 | $1,387.46 |

| 33 | Texas | 6.25% | 1.62% | $176,700 | 91.2 | $1,384.80 |

| 34 | Minnesota | 6.88% | 1.09% | $220,600 | 99.7 | $1,529.58 |

| 35 | South Dakota | 4.50% | 1.19% | $181,700 | 99.5 | $1,372.81 |

| 36 | Kansas | 6.50% | 1.26% | $128,400 | 90.2 | $1,483.57 |

| 37 | Missouri | 4.23% | 0.96% | $147,400 | 89.9 | $1,386.16 |

| 38 | West Virginia | 6.00% | 0.51% | $103,500 | 95.9 | $1,379.58 |

| 39 | Illinois | 6.25% | 1.97% | $170,700 | 97.2 | $1,440.44 |

| 40 | New York | 4.00% | 1.35% | $262,000 | 132.5 | $1,459.41 |

| 41 | New Jersey | 6.63% | 2.14% | $316,700 | 121.9 | $1,583.61 |

| 42 | North Dakota | 5.00% | 0.90% | $206,500 | 99.7 | $1,403.90 |

| 43 | Maine | 5.50% | 1.23% | $219,300 | 113.6 | $1,321.86 |

| 44 | New Mexico | 5.13% | 0.65% | $183,500 | 94.9 | $1,331.83 |

| 45 | Alaska | 0.00% | 0.97% | $289,100 | 131.3 | $1,373.02 |

| 46 | Nebraska | 5.50% | 1.60% | $157,800 | 92.9 | $1,446.83 |

| 47 | Montana | 0.00% | 0.75% | $215,800 | 100.4 | $1,334.60 |

| 48 | Connecticut | 6.35% | 1.66% | $261,700 | 125.7 | $1,599.27 |

| 49 | Rhode Island | 7.00% | 1.51% | $276,000 | 123.6 | $1,461.27 |

| 50 | Vermont | 6.00% | 1.76% | $224,300 | 120.7 | $1,465.34 |

Click through to learn how much you need to survive retirement.

More on Retirement Planning

- 50 Cheapest Places to Retire

- 15 US Cities You Should Really Consider for Retirement

- How Much You Need Saved for Retirement in Every State

- Watch: How One Couple Retired in Their 30s to Travel in an Airstream RV

We make money easy. Get weekly email updates, including expert advice to help you Live Richer™.

Methodology: GOBankingRates ranked all 50 states based on four main factors affecting retirees: taxes, living expenses, banking, and healthcare and Social Security. These four factors were broken down into sets of data points, each of which was scored on a scale of 0 to 1 and then combined with weighting for the overall score. In the taxes category, we examined: (1) average state sales tax rates, sourced from the Tax Foundation; (2) average property tax rates, sourced from the Tax Foundation; (3) property tax rate, sourced from the National Association of Home Builders; and (4) state taxes on Social Security benefits, sourced from Kiplinger and weighted twice as much as property taxes, four times as much as average state sales tax and one-half more than property tax rate. In the living expenses category, we examined: (1) the median home listing price, sourced from Zillow the week ending May 10, 2018; (2) median home values, sourced from Zillow’s April 2018 data; and (3) each state’s cost-of-living index value, where the U.S. average is 100, sourced from the Missouri Economic Research and Information Center, which was weighted twice as much as median listing price and four times as much as median home value. In the banking category, we examined: (1) savings account interest rates, sourced from GOBankingRates’ database, and (2) two-year CD account interest rates, sourced from GOBankingRates’ database, with both data points weighted one-quarter as much as the other factors.In the healthcare and Social Security category, we examined: (1) average health insurance premiums, sourced from the Kaiser Family Foundation, and (2) average Social Security benefits, sourced from the Social Security Administration, with the average Social Security weighted twice as much as average health insurance premiums.

Funds — How To Find Out If Any of It Is Yours?")