Social Security in 2022: Many Americans Feel They’re Lacking Education on It — Here’s a Quick Guide

Written by

Yaël Bizouati-Kennedy

Written by

Yaël Bizouati-Kennedy

Edited by

Molly Sullivan

Edited by

Molly Sullivan

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

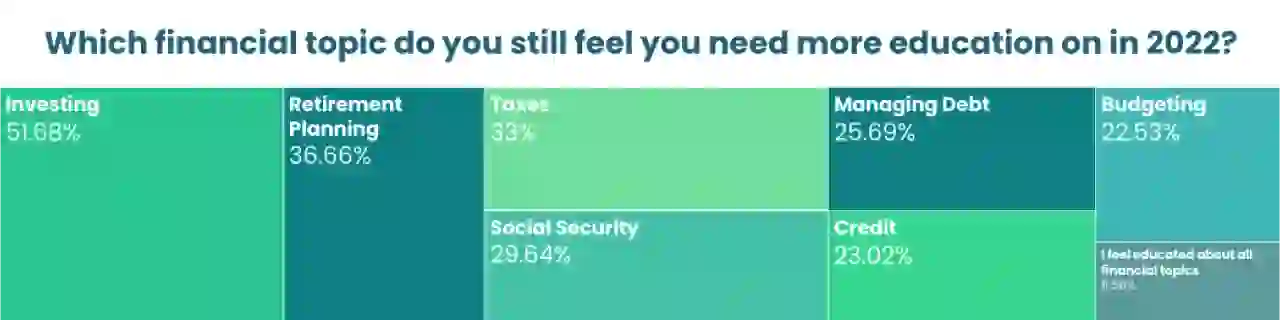

Social Security, designed to pay retired workers, is a continuing income after retirement and covers about 64 million Americans, according to its website. However, despite how much you hear about Social Security in the news, a new survey finds that 30% of Americans still feel they need more education on the topic.

The new GOBankingRates survey finds, interestingly, that the generation saying they need more education about Social Security the most is the 55 to 64 age group, with 40%. This is followed by both the 18 to 24 age group, and the 25 to 34 age group with 34%.

Considering that, on average, Social Security retirement benefits replace 40% of pre-retirement income for retirement beneficiaries, it’s never too early to understand how it works and which special situations you should be aware of.

Dan Demian, financial advice expert at banking app Albert, told GOBankingRates that Social Security is essential to understand, because if you’re not saving for retirement, Social Security payments may be your only source of income once you’ve stopped working and what you earn during your working years affects how much you may get paid in retirement.

“Your social security payment isn’t a sure thing. It depends on several factors, such as your average income, years worked, and the social security trust balance, which may change. So it would be best if you planned to save for your retirement independently,” he said.

If you feel like you’re lacking some knowledge about Social Security, here are some of the most important issues to understand.

How You Qualify

In order to qualify for Social Security benefits, you need to be 62 or older, or disabled or blind, and “insured” by having enough work credits.

In addition, for applications filed on Dec. 1, 1996, or later, you must either be a U.S. citizen or lawfully present alien in order to receive monthly Social Security benefits, according to the Social Security website.

Americans start their eligibility by working and paying Social Security taxes, either through payroll deductions (required by the Federal Insurance Contributions Act, or FICA) or through income tax filings if you are self-employed (required by the Self-Employed Contributions Act, or SECA), AARP explains.

You qualify for Social Security by compiling credits when you pay Social Security taxes on your earnings. You can earn up to four credits per year. Workers qualify for Social Security retirement benefits when they reach 40 lifetime credits, AARP adds.

How Much You Get

Social Security benefit payments depend on how much you earned during your working career. Higher lifetime earnings result in higher benefits. If there were some years you didn’t work or had low earnings, your benefit amount may be lower than if you had worked steadily, according to SSA’s Social Security Matters website.

It’s important to know that you can get Social Security retirement benefits as early as age 62. However, the benefits will be reduced. When you delay benefits beyond your full retirement age, the amount of your retirement benefit will continue to increase up until age 70.

Special Situations

“It’s not the first thing that will come to mind after a traumatic event, but the death of a spouse (or ex-spouse, or a parent if you are under 18) has implications for when (and for how much) you can claim the survivor benefit,” Jason Vissers, financial analyst, MerchantMaverick.com, told GOBankingRates. “Likewise, if you become disabled or seriously ill and cannot work, you’ll need to become familiar with how SSDI benefits work.”

The SSA explains that widows and widowers may qualify if he or she is:

- Age 60 or older; or

- 50 or older and disabled; or

- Divorced, age 60 or older (age 50 if disabled), and was married to the other person for at least 10 years prior to divorce; or

- Under age 60 and caring for the former couple’s child (under age 16 or disabled prior to age 22) and who is entitled to child’s benefits; or

- Divorced, under age 60 and caring for his or her child (under age 16 or disabled prior to age 22) who is entitled to benefits on the other person’s record

Another potentially confusing scenario is divorce, Ted Rossman, senior industry analyst, CreditCards.com, told GOBankingRates.

“You can potentially claim benefits based upon the working records of an ex-spouse as long as you were married 10 or more years,” he said. “In all cases, it’s important to run the numbers. For example, should you claim based upon your own working record or your spouse’s (or ex-spouse’s)? When should you claim? And so on. It’s a big decision, so don’t be afraid to ask questions and enlist the help of a professional if needed.”

To be eligible for the Social Security’s divorced spouse benefits benefit program, you must meet the following requirements:

- Be at least 62 years old and not currently married

- Be divorced from a person who receives Social Security retirement or disability benefits

- Have been married to that person for at least 10 years before the date the divorce became final

- Not be entitled to an equal or higher retirement or disability benefits

In any case, Rossman said that it’s definitely important to undestand how Social Security works the closer you get to retirement age.

“If you’re currently in your 20s, 30s or even 40s, I wouldn’t put a ton of thought into Social Security because a lot could change between now and when you’re eligible for benefits,” he said. “Once if you’re in your 50s or 60s, though, then it’s very important to understand what Social Security means for you. It’s confusing and I’m not surprised that many people have questions. The more complex your situation, the more you might benefit from a consultation with a financial advisor.”

More From GOBankingRates

Methodology: GOBankingRates surveyed 1,012 Americans aged 18 and older from across the country on between March 8 and March 9, 2022, asking sixteen different questions: (1) Do you consider yourself financially literate?; (2) Where did you learn most of your financial literacy?; (3) Which financial topic do you think you should have learned more about in high school? (Select all that apply); (4) Which financial topic do you still feel you need more education on in 2022? (Select all that apply); (5) When you were growing up, did your parents talk to you about how to manage your money?; (6) Do you think high schools are lacking in financial education?; (7) How has a lack of financial education cost you the most?; (8) At what age did you become comfortable with basic money skills (i.e., writing a check, balancing your accounts, budgeting)?; (9) At what age did you start saving and planning for retirement?; (10) How do you feel about how you used your 2021 American Rescue Plan stimulus check?; (11) Which financial topic did you feel the need to learn more about due to the COVID-19 pandemic? (Select all that apply); (12) What do you not understand about the Child Tax Credit? (Select all that apply); (13) Which part of the homebuying process is most confusing to you?; (14) Which part of the car buying process is most confusing to you?; (15) Are you prepared for the student loan debt moratorium to end in May?; and (16) How are you changing your driving habits with the rising gas prices? GOBankingRates used PureSpectrum’s survey platform to conduct the poll.

")