Is a Self-Directed IRA Right for You?

Written by

Joel Anderson

Written by

Joel Anderson

Edited by

River Jean-Noel

Edited by

River Jean-Noel

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

With a dizzying array of stocks, bonds and funds available, determining what to put in your IRA can be a pretty daunting task; there are simply too many options. However, for a certain group of investors, the exact opposite is true. The gamut of investment products offered through a traditional broker might not prove satisfactory for a select few investors.

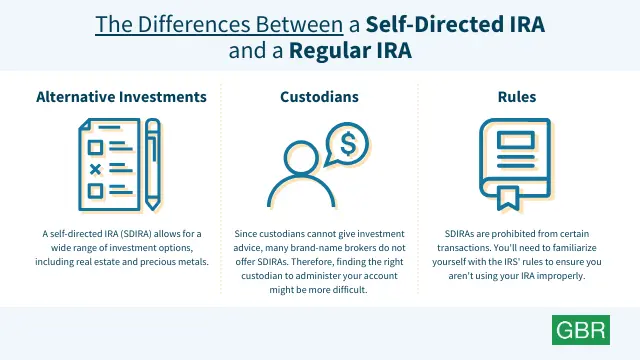

If you want to build a portfolio with nontraditional investments but still get the tax-advantages offered by a regular IRA, you have an important tool in the self-directed IRA (SDIRA). An SDIRA is an IRA that allows you to invest pre-tax money in nontraditional assets like real estate, private equity or precious metals.

- What Is a Self-Directed IRA?

- Where Can I Get a Self-Directed IRA?

- Is a Self-Directed IRA Right for Me?

- Pros and Cons

- Summary — What Can You Expect?

- FAQ

What Is a Self-Directed IRA?

A self-directed IRA is similar to a traditional IRA with one major exception: the types of investments you put into it.

While the annual contribution limits for SDIRAs are the same and you’re contributing pre-tax income — allowing you to write contributions off on your taxes — most regular IRAs are limited to holding traditional types of assets, like stocks and bonds.

Self-directed IRAs, however, allow owners to invest in a wider range of assets. Some alternative investments you can hold in an SDIRA include real estate, precious metals and stocks in private companies. Therefore, self-directed IRAs might be the right type of investment vehicle for nontraditional investors who can’t access the tax advantages offered by more traditional retirement accounts, like a 401(k) or an IRA.

With a self-directed IRA, you can opt for the traditional or Roth variant to make contributions from your pre-tax or after-tax income, respectively. From there, a self-directed IRA functions much like a regular IRA — with income from the investments staying in the fund until you start taking your required minimum distributions in retirement.

Another major difference is in the role of the plan custodian or trustee. A custodian administers your plan, reviews your potential assets and acquires the assets for the account. The custodian isn’t some sort of gatekeeper or de facto financial advisor; they won’t do research for you or manage your account. Your custodian will either rubber stamp an investment as being legal and permitted by the plan or reject the potential investment, so don’t expect them to protect you from poor or risky investments.

While some custodians will administer just about any investment you can think of, there are some items no IRA can hold. These include life insurance and “collectibles” — a broad catch-all category that includes everything from stamps to rare coins

Where Can I Get a Self-Directed IRA?

Setting up an IRA — Roth or traditional — is abundantly easy, with myriad options for brokers and banks that will administer your plan. The self-directed route is a bit trickier. The one main thing you’ll need to do is to begin by finding a custodian or administrator to manage the account.

The firms where you can set up a self-directed IRA aren’t going to be the household names you’re used to seeing. It’s an extremely niche product, so you’ll have to find firms that will help you set one up and act as custodian — a service you will often have trouble getting a big-name broker to provide. That means going to places like EquityTrust, The Entrust Group or the Pensco Trust Company.

The custodians can set the parameters for which legal assets can be included, so you need to spend some time shopping around to ensure you’ve found the right custodian for you. The good news is that — given they can’t provide financial advice — your only consideration is cost and the types of assets they allow.

Is a Self-Directed IRA Right for Me?

In a word, no. Investing in nontraditional assets is a difficult, risky process that requires an enormous amount of research on your end if you want to do it right. Certainly, if you’re already flipping houses or investing in private equity successfully, an SDIRA could be a great addition to your financial planning because it gives you a chance to limit the tax liabilities on activities you’re already taking part in. However, if you aren’t already an experienced and knowledgable investor in a specific nontraditional asset, the SDIRA won’t benefit you much.

There are also traditional securities that will allow you to make almost all of the same investments indirectly. While you might consider the ability to branch out into real estate or precious metals an important way to diversify your portfolio, the truth is you can do that using traditional securities that won’t require a specialized retirement account. You might not be able to buy up an apartment building, but you can own a real estate investment trust (REIT) that represents a collection of similar properties and pays you a dividend based on the rents. You might not be able to buy gold bullion, but you can certainly invest in gold futures or exchange-traded funds (ETFs) designed to track the price of gold. As such, the degree to which you can improve your diversification with an SDIRA is relatively limited given just how detailed and specific the myriad options within the world of traditional, can-go-in-your-normal-IRA securities. You can make essentially the same bets with financial products that are allowed in a regular IRA, just less directly.

So, unless you’re already someone with plenty of experience and knowledge about a particular asset type that falls outside the purview of regular IRAs, you probably don’t need to give a lot of thought to opening an SDIRA.

Find Out: How Much You Should Have in Your Retirement Fund at Every Age

Pros and Cons

The pros of using an SDIRA come down to two things: diversification and avoiding taxes. As noted above, if you’re already making money investing in nontraditional assets, opening an SDIRA is an easy way to get a tax write-off for the investing you’re already doing. Whether you opt for a traditional SDIRA or a Roth SDIRA, you’ll be able to grab all the same tax benefits as other IRAs.

What other IRAs can’t do is provide the same level of diversification as an SDIRA. While you can replicate almost all of that diversity with securities, you can never be completely certain of how markets will pan out. Expanding the number of different types of investments you’re holding means you’re that much more protected from risk.

As for the cons of having an SDIRA, it’s important to know just how complex and strict the rules surrounding them can be. In particular, the chance that you might engage in “self-” or “double dealing” — i.e., deriving direct personal benefits from your investments.

If you’ve bought a hotel with your SDIRA and decided to stay there for a night free of charge, you would be engaging in double-dealing. Once you comp your room, you’ll have to close out your entire SDIRA and distribute its holdings i.e. pay taxes on the value of the entire account as income and an additional 10% tax penalty for pulling out early. A pretty massive tax hit, all told, for someone who was just trying to save some money on a hotel stay.

And even a minor slip up with this rule or any others can result in the entire account being “distributed.” This means you’ll have to declare the entire value of the account as taxable income in that year and pay a penalty for the prohibited transaction. Such a slip up can easily result in a tax hit of 40% to 60% when all is said and done.

Summary

An SDIRA is a specific type of retirement account that offers very narrow benefits to a small class of investors. For the average retirement investor, a traditional mix of stocks, bonds and funds is more than enough to build a diversified portfolio that truly limits your exposure to any single risk.

However, if you do have the sort of specialized knowledge about an asset class that falls outside what regular IRAs accept, an SDIRA might allow you to continue investing in those asset types and get the same tax benefits you would from a traditional IRA or Roth IRA.

FAQ

Here are some quick answers to some frequently asked questions about SDIRAs:

What is an SDIRA?

A self-directed IRA is a form of IRA that allows for the inclusion of nontraditional types of assets like owning real estate, private equity or precious metals.

Who needs an SDIRA?

Retirement investors who are knowledgeable about a certain asset class and want the ability to access the tax benefits of an IRA. Unless you’re already successfully investing in a certain type of asset that’s not allowed in a regular IRA, an SDIRA is most likely not going to be of much benefit.

What can go into an SDIRA?

Each SDIRA custodian will have their own types of assets that can be included, but almost any investment or asset can hypothetically be included. The exceptions would be a few asset types specifically barred from inclusion, like life insurance or collectibles.

How do I set up an SDIRA?

You’ll have to shop around for a custodian before opening an account. Most potential custodians are specialists that focus on providing services surrounding an SDIRA. Keep in mind that an SDIRA custodian will not offer you financial or investment advice.

What are the potential drawbacks?

The types of assets that you can’t put into a regular IRA are usually much riskier than the securities packaged with the investor in mind. And even if you find less risky assets, a minor violation of the rules can result in the entire account being distributed with a hefty tax penalty.

What is “self-dealing?”

You’re not allowed to receive any direct benefits from the assets held in your SDIRA. So, if you own a rental property you’re technically in violation of the SDIRA’s rules if you spend a night there.

More From GOBankingRates

- Best Online Brokerages of 2019-2020

- Best Online Stock Brokers for Beginners 2019-2020

- Best Roth IRA Providers 2019-2020

- Best IRA Providers of 2019-2020

Funds — How To Find Out If Any of It Is Yours?")