44% Pay Off Their Full Credit Card Balance, Survey Finds: Pros and Cons of This Strategy

Written by

Andrew Lisa

Written by

Andrew Lisa

Edited by

River Jean-Noel

Edited by

River Jean-Noel

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

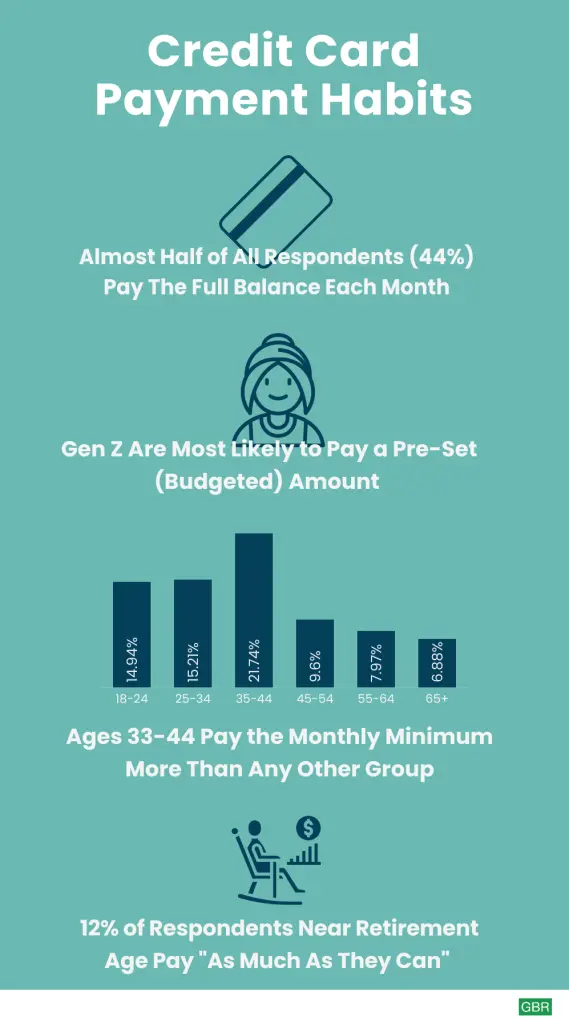

GOBankingRates recently surveyed more than 1,000 American adults about their credit-card habits — and the results revealed some promising trends. The largest group of respondents by far paid off their credit card bills in full each and every month. Everyone knows that it’s irresponsible to charge purchases that you don’t have the cash to cover, so paying the total balance every billing cycle is a good thing, right?

In concept, yes. But the reality on the ground is a little more complicated than that.

Read: How Credit Card Use Changed During the Pandemic

Nearly Half Pay Their Bill in Full Every Time

The survey asked respondents, “Wow do you handle your credit card bill every month?” Here’s a look at the responses:

- 0.79% use autopay or a third-party app

- 6.54% pay a set amount every month

- 9.12% pay off as much as they can

- 13.38% make only the minimum payment

- 26.07% pay more than the minimum but never the full balance

- 44.10% pay it off completely

Men are less likely than women to pay only the minimum balance and more likely to pay off their bills in full every month, but only by a few percentage points. Young people are much more likely to pay only the minimum, but in terms of paying the whole bill every month or not, there’s a remarkable consistency between all age groups.

Find Out: Which Is Smarter: ‘Buy Now, Pay Later’ or Credit Cards?Closing a Credit Card? Here’s What You Should Do Instead

So, which group is doing it the right way — the 44% who pay their entire bill every month or the 56% who do not?

Well, that depends.

It’s Important to Understand Which ‘Bill’ You’re Talking About

Every month when your billing cycle ends and your due date nears, you’ll get a bill that includes two payment amounts:

- Statement balance: This is the sum of all charges that post by the day your billing cycle ends.

- Current balance: This is the sum total of all the money you owe on your credit card, including charges from your previous statement and any pending charges that will get pushed to your next statement.

Read: Jaw-Dropping Stats About the State of Credit Card Debt in America

See: Why It’s Still Better To Use Your Credit Card Over Your Debit Card

Paid Statement Balances Equal Healthy Credit

It doesn’t always make sense to pay your entire current balance — more on that in a moment — but when it comes to your statement balance, there aren’t a lot of solid arguments for paying anything but the full amount. When you pay your statement balance each and every time, you avoid being hit with finance charges. That’s the interest that the bank collects for extending you the line of credit in the first place.

Credit card interest compounds daily and the average APR ranges from around 15% to deep into the 20s. Those hefty finance charges quickly transform small debts into big debts and negate the value of any rewards, miles, cash back, or points you might have earned along the way.

Find: The Riskiest Places To Swipe Your Credit Card

If you slip up and pay less than your statement balance even once, you’ll have to pay in full two months in a row to catch back up.

The only time it would make sense to pay less than your statement balance is if doing so would stretch you so thin that you might not be able to pay your other bills. But that only happens if you charge purchases that you don’t have the cash to cover — one of the biggest no-nos from Credit Cards 101.

Paying Your Current Balance Might Help Your Credit Score

Your current balance is always at least as high or higher than your statement balance, so if you’re struggling to pay the latter, the former will stretch you even thinner.

But even if you can pay it all without compromising your budget, what’s to be gained? Maybe a bump to your credit score.

Find out: Why Using a Credit Card Doesn’t Mean You’re Going Into Debt

Paying the statement balance alone gets you off the hook for finance charges and interest payments — you won’t do any better on that front whether you satisfy your current balance or not. When your lender reports your payment, however, the credit bureaus will recalculate your all-important credit-utilization ratio. That’s the amount of your available credit that your using — less is always better.

If you pay your current balance in full, your credit utilization ratio will be a perfect zero. If you pay only your statement balance, your credit utilization ratio will be the percentage of whatever is left over on your bill.

If that amount pushes your utilization above 30% — the standard benchmark for healthy credit — then you might want to pay the whole thing. The same also holds true if you’re applying for a loan and want to show zero debt.

Beyond that, only you can decide if your financial life has squeakier wheels that are more deserving of a little TLC.

The Money Might Be Better Spent Elsewhere

Paying your statement balance keeps you above water. If there’s any money left over, should you spend it on settling your full current balance just to see a temporary and probably negligible bump in your credit score?

Read: How Many Credit Cards Should I Have, Anyway?

Only you can answer that. But keep in mind that every dollar you spend on your current balance when you don’t really have to is a dollar you’re not:

- Investing in the stock market

- Contributing to your emergency fund

- Saving for retirement

- Putting into your home, education, or quality of life

One thing is sure. The 13.38% of respondents who reported making only the minimum payment are doing it wrong. By stringing out their debt and interest payments as long as legally possible without actually going into default, they make themselves the bank’s favorite customer. Pay your statement balance every time and you’ll beat the bank at its own game. The value in paying your current balance, on the other hand, is not nearly as cut and dry.

GOBankingRates surveyed 1,009 Americans aged 18 and older from across the country on September 22 through September 23, 2021, asking twelve different questions: (1) Which of the following is the most important to you when it comes to picking a new Credit Card?; (2) How do you handle your Credit Card bill each month?; (3) Which Credit Card company do you trust the most?; (4) What age did you get your first Credit Card?; (5) What is your primary purpose for using your Credit Card(s)?; (6) Do any of the following statements apply to you? Select all that apply:; (7) Which Credit Card fees do you hate the most? Select one:; (8) How many Credit Cards do you own?; (9) What is your total current Credit Card debt?; (10) How Long do you think it will take you to pay off your Credit Card debt?; (11) Have you ever hit the credit limit on your Credit Card?; and (12) Have you ever charged any of the following to your Credit Card? Select all that apply: All respondents had to pass a screener question of: Do you own/use a Credit Card(s)?, with an answer of “Yes”. GOBankingRates used PureSpectrum’s survey platform to conduct the poll.