How Mortgage Rates Are Impacting Sellers

Written by

Andrew Lisa

Written by

Andrew Lisa

Edited by

Levi Leidy

Edited by

Levi Leidy

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

Many factors contributed to the historic seller’s market that endured throughout the pandemic, which saw home prices rise by more than 50% in two years in some states. One of the biggest drivers of that growth was dirt-cheap mortgage rates.

“The low interest rate environment has created an unprecedented opportunity for not only buyers getting a great rate but homeowners seeing the value of their homes increase exponentially,” said Bill Gassett, founder of Maximum Real Estate Exposure.

Buyers, Beware: 10 Extra Homebuying Costs You’re Probably Forgetting About

The environment that made that dynamic possible for all these months, however, is slowly fading away.

“While real estate markets don’t change overnight,” Gassett said, “there is a very strong chance that, with the Fed’s increase of rates multiple times in the coming year, real estate markets will eventually change.”

Rates are rising and the market is changing. Here’s what it means for sellers.

Buyers Can’t Afford as Much Home

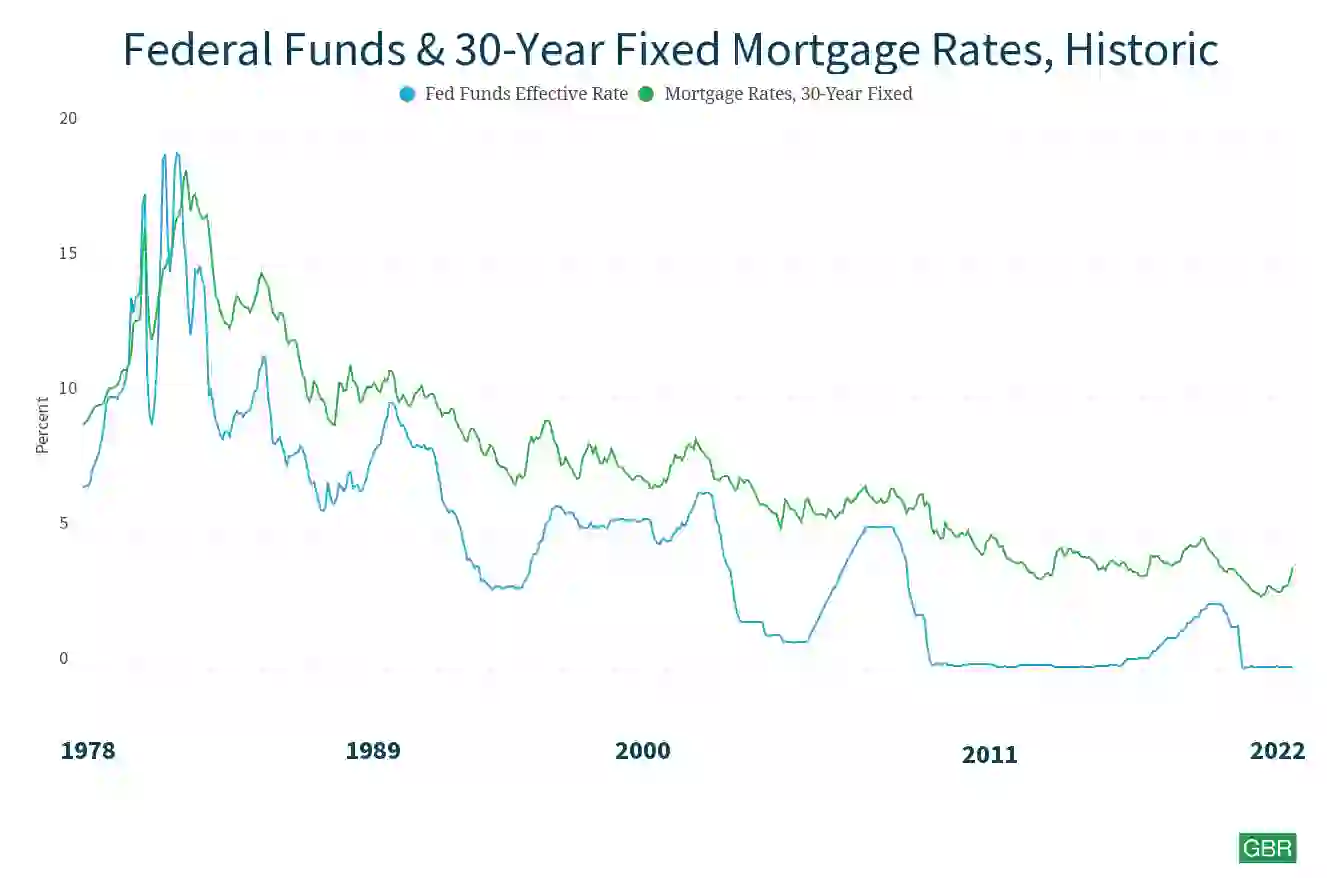

Make no mistake about it: Mortgage rates are rising in 2022 — and they’re rising quickly.

“Only last week, the 30-year mortgage rate was 4.16%,” said WeLoans CEO Lucia Jensen. “In just a week’s time, the rate is up to 4.47%, representing a 0.31% jump in seven days.”

Every added basis point on the interest rate drives down the amount of money that buyers can borrow — and therefore reduces the amount of house they can afford.

“Effectively, increased mortgage rates reduce conventional buyers’ buying power by 9% to 10% to 11%, pending their debt-to-income ratio,” said Baron Christopher Hanson of Echo Fine Properties. “Pre-approved buyers for $500,000 to $1 million in mortgage funding can see their purchasing power reduced by $45,000 to $110,000 based on a rise in mortgage rates. This cooling of traditionally financed buying power across the board ultimately puts pressure on sellers hoping to earn top dollar on their homes.”

When Buyers Can’t Buy as Much, Demand Falls

On March 18, the National Association of Realtors reported that home sales fell in February by 7.2% — much more than expected — to a six-month low. While it’s too early to diagnose a definitive cause and effect, it’s impossible to ignore that rising rates immediately preceded a steep decline in demand.

“Current mortgage rates are making it less affordable to buy a home,” said Adrian Brikho, senior mortgage advisor at Brik Home Loans. “Buyers who were on the edge of qualifying are going to get priced out of the market. We’re going to see a slowdown in demand in the coming months, which will affect the price a seller can get for their home.”

When Demand Falls, Sellers Have to Lower Prices — Usually

Rising rates reduce demand; and, when demand falls, prices should, too.

“It’s important to remember that there is a consistent correlation between interest rates and home prices,” said Ward Morrison, president and CEO of Motto Franchising, LLC. “When interest rates increase, affordability of homebuying decreases, causing an inverse reaction to home valuation. To offset this issue, the market stabilizes and home prices go down.”

That pattern is what you could expect in a normal year, but 2022 is no normal year.

“Luckily for home sellers,” Morrison said, “because real estate supply and demand is so off balance right now, we likely won’t see prices decrease as rapidly as we have in the past.”

Demand Might Rise Before It Falls for Real

Many experts are expecting demand to spike momentarily before falling once again. You can chalk it up to buyer FOMO.

“In today’s current climate, with the expectation that interest rates will continue to rise, and with interest rates still remaining low from a historical context, I believe the desire to lock in low interest rates will only gather a greater sense of urgency,” said Michael Rehm, a licensed real estate agent in Sacramento, California. “This will cause more buyers to get off the sidelines and into the market, only increasing the demand and the prices of homes overall, which will benefit the sellers in today’s market.”

Sellers Should Expect More Headaches From Empowered Buyers

As rates rise, demand slows and prices fall, the balance of power will slowly shift from the seller to the buyer — and buyers soon will be able to make demands that would have pushed them out of the running in the red-hot days of the 2021 bidding wars.

“Increased mortgage rates will also temper the volume of buyers willing to forgo inspection periods and invest 4% to 6% to 8% of the home’s appraised value in punch-list improvements that sellers were able to ignore during the COVID real estate buying frenzy,” Hanson said.

Sellers also are likely to be frustrated by buyers who were pre-approved based on numbers that the lender crunched prior to the interest rate hikes.

“As interest rates rise, home sellers also need to factor in the buyer’s ability to afford a home and ensure that their mortgage preapproval is based on current interest rates,” Morrison said. “This is crucial; because, if a seller accepts an offer from a buyer who was preapproved at a lower rate and no longer qualifies, that’s valuable time and money lost on the transaction.

“To prevent this, it is wise for sellers to work with a buyer who has lending options — like a mortgage broker, for instance, who can shop on behalf of the buyer to provide a variety of options.”

Most Sellers Will Have to Become Buyers Themselves

The most important thing for sellers to remember is that, unless they have a spare house, they become buyers when the deal is closed.

“I’ve been hearing more and more current homeowners say, ‘I could sell, but what would I be able to buy? I couldn’t afford to buy my own house in this market,'” said Matthew Posey, residential mortgage loan originator with Axia Home Loans. “The current real estate scales are firmly tipped in the seller’s favor and not the buyer’s. The net benefit to a seller who goes on to purchase another home is diminished when the scales are tipped too far to either side. That’s why professionals in the housing market, myself included, always prefer a balanced market where both buyers and sellers benefit.”

More From GOBankingRates