Term vs. Whole Life Insurance: How To Know Which One You Need

Written by

John Csiszar

Written by

John Csiszar

Edited by

Molly Sullivan

Edited by

Molly Sullivan

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

Life insurance is frequently overlooked as part of a financial plan, but it can be a critical addition to your basic financial security. Part of the reason why life insurance is often maligned is that it can be hard to understand. But the basic concept is that your life insurance policy will protect you and your family against financial loss in the event you die, which is particularly important if you are the family’s primary breadwinner.

While you should speak with a life insurance specialist or financial advisor before you commit to a policy, here is what you’ll need to have a basic understanding of when it comes to the difference between the two primary types of life insurance, term and whole.

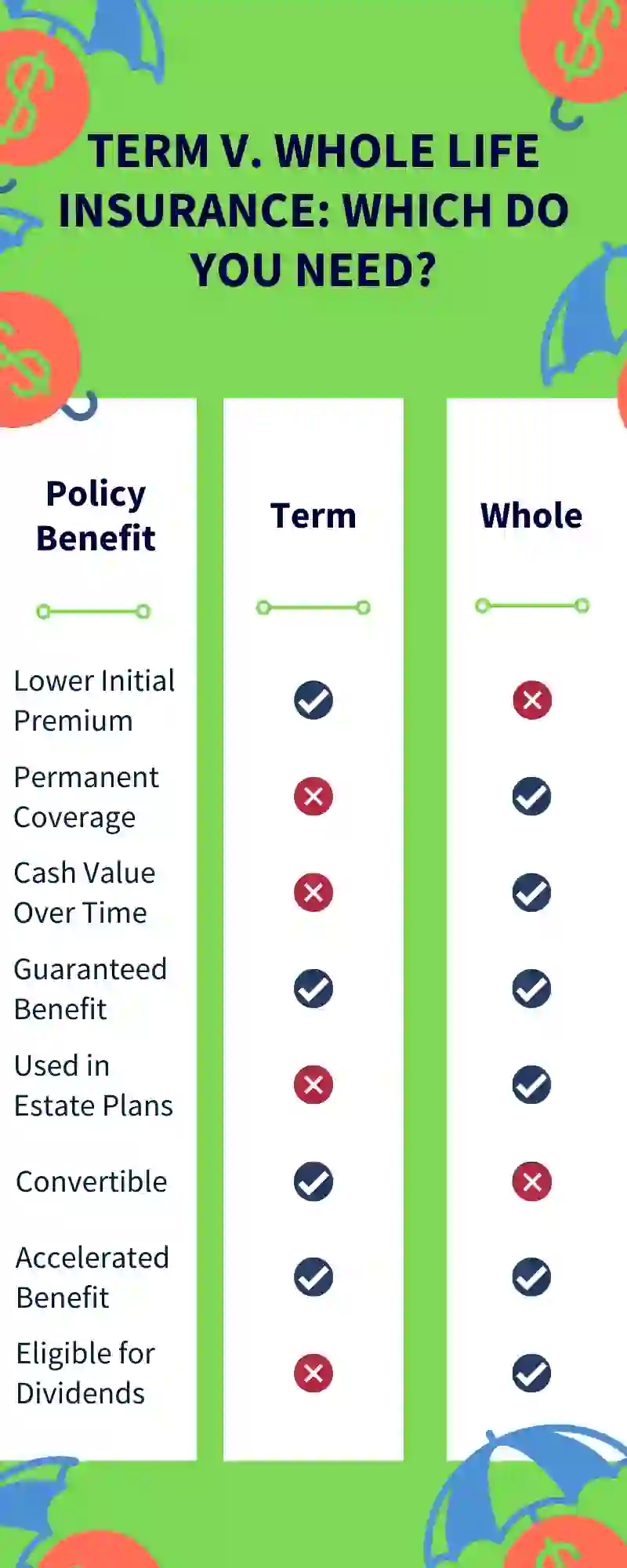

Basics of Term Life Insurance

Term life insurance is the most inexpensive and the most straightforward type of life insurance. As the name suggests, term life insurance only protects you for a specified length of time, often 10 to 30 years. There are few added bells and whistles with most term life policies. Your premium goes entirely toward the cost of your insurance, including policy fees and charges, and there is no investment component involved. You can usually choose whether you want a level premium over the entire course of your term or whether you want your policy to be continually renewable, possibly at varying prices.

Term life can be significantly less expensive than whole life because it only provides coverage for a limited time and doesn’t offer much by way of additional perks.

Basics of Whole Life Insurance

Whole life insurance lasts for your entire life, rather than just a specified term. But there are many more aspects to whole life insurance that make it very different from term insurance. Overall, whole life insurance is more like an investment than the simple insurance coverage offered by term life.

When you put money into whole life insurance, your premium goes into three separate components:

- The cost of insuring you

- The fees and charges of the policy itself

- The policy’s cash value

With a whole life policy, a portion of your policy is invested and earns a guaranteed minimum amount. In most policies, you can borrow against or even withdraw at least a portion of the cash value. You can also get the entire cash value if you surrender your policy, although there are likely to be high fees and penalties if you surrender your policy within the first several years after purchase.

Who Benefits Most From Term Life Insurance?

Term life insurance is best suited for those that want the lowest-cost insurance available and need coverage for a specified time only.

For example, if you only want insurance until your kids are through college or until your mortgage is paid off, you might prefer buying a 20- or 30-year term policy. This will be the lowest way to get insurance during the time that you most need it.

It’s also the best option for those looking for the maximum possible insurance payout for the lowest possible cost. Term life insurance only pays off if you die while the policy is still in force, meaning there is a decent chance that the insurance company won’t have to pay you anything at all. The reason a whole life policy costs more is because if you hold that policy for your entire life, the insurance company will ultimately be required to pay off the death benefit.

Who Benefits Most From Whole Life Insurance?

Whereas term policies don’t offer any cash value or payout after the covered period expires, whole life offers an investment component that grows over time, along with a permanent death benefit. Whole life policies are best for those who want constant insurance for their entire lives at a steady premium.

This feature can be important if you either have a health problem or anticipate encountering poor health, as your insurance will remain in force and your premiums won’t increase regardless of your condition. You can also use the cash value component to pay premiums if you can’t afford them, or to borrow against or even withdraw those funds if you need the money. The tradeoff is that your whole life policy could cost significantly more than a term policy.

More From GOBankingRates