How Do Bank Loans Work? Types, Requirements and Approval Tips

Written by

Sarah Sharkey

Written by

Sarah Sharkey

Edited by

Nupur Gambhir, CFHC™

Edited by

Nupur Gambhir, CFHC™

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

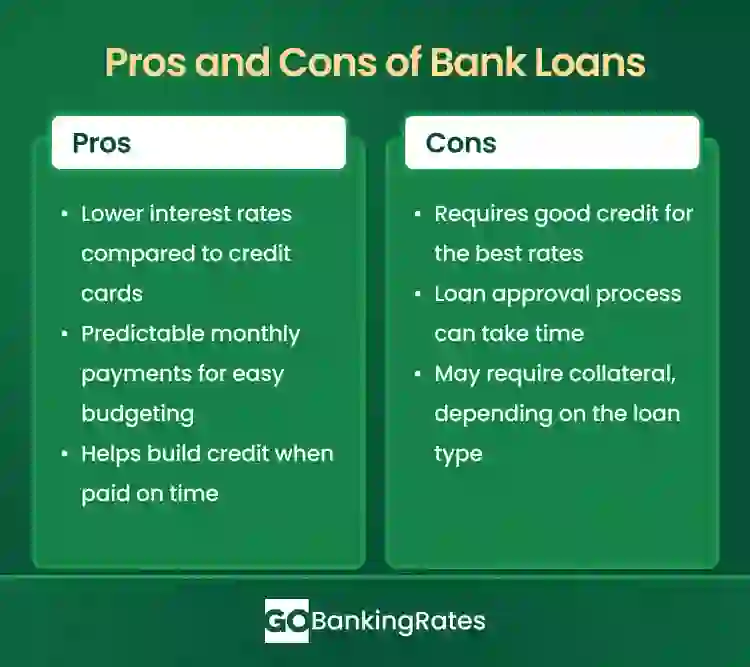

A bank loan might be the best solution when you need to borrow money to make a large purchase or to cover unexpected expenses. There are several different kinds of personal bank loans, such as auto loans and personal lines of credit.

Determining why you need the loan and how quickly you will be able to repay it can help you decide which type of loan is right for you. To save money over the life of the loan, take time to research and find the best personal loan rates. We explore how bank loans work today.

Types of Bank Loans

There are a variety of personal loans available through banks. If you are buying a car, you will apply for an auto loans. If you need money for other reasons, you might apply for a personal line of credit. If you want to access the equity in your home, you might take out a line of credit against your home, called a home equity loan. These all tend to be secured loans. Banks might also offer unsecured personal loans. Credit unions typically offer the same types of loans, sometimes at lower rates.

Take a look at some of the most common types of bank loans below:

- Personal loans. The funds from a personal loan can be used to cover almost any purchase. You might use the funds for debt consolidation, medical bills, home repairs, celebration expenses, and more. Although many personal loans are unsecured, some personal loans require collateral.

- Auto loans. An auto loan can be used to purchase a vehicle. Typically, an auto loan is secured by the vehicle you purchase with the funds.

- Mortgage loans. Banks offer mortgage loans to help a borrower pay for a home purchase. Typically, these large loans come with loan repayment terms of 15 to 30 years with either fixed or adjustable interest rates. Your home serves as the underlying collateral, which means if you cannot keep up with the mortgage payments, the bank might foreclose on your property.

- Business loans. Many banks offer business loans to both small and large businesses for any number of business expenses. Depending on the situation, the loan might be secured by business assets or unsecured.

- Student loans. Some banks offer private student loans to help students pay for educational expenses, like tuition, books, and living expenses. Unlike federal student loans, private student loans don’t offer attractive borrower protections, like student loan forgiveness or income-based repayment options.

Regardless of the loan type, a bank loan is a sum of money you borrow from a bank or a credit union. The bank will issue the loan based on your credit rating and current ability to repay the loan. The monthly payments will go to the bank, and the interest rate is usually determined by your credit score.

How the Bank Loan Process Works

Although the specifics of obtaining a bank loan vary slightly from financial institution to financial institution, the overall process tends to look similar. Below is a look at how the process usually works:

- Loan application. The process starts when you submit a loan application. Be prepared to share information about your income, employment, credit history, and loan purpose.

- Credit evaluation. Banks will review your situation, including looking at your credit score, financial history, and debt-to-income ratio.

- Loan approval or denial. Depending on the bank’s evaluation of your application, they will approve or deny the loan request. Alternatively, the bank might request more information about your situation.

- Loan terms and agreement. If you are approved for the loan, the bank will send over documents outlining the loan terms, interest rates, repayment period, and fees. It’s important to carefully review this information to confirm you are comfortable with the details of the loan before moving forward.

- Loan disbursement. If you accept the loan, the funds might be disbursed as a lump sum or line of credit.

- Loan repayment. Once you receive the loan, you’ll start making payments based on your loan terms. In many cases, you might make regular monthly payments of principal and interest. If you want to repay the loan early, that’s often an option. But check into prepayment penalties before moving forward.

Before starting the process with any particular bank, it’s a good idea to shop around to find out which bank offers the lowest interest rates and fees.

Secured vs Unsecured Bank Loans

The loans can be secured — attached to collateral like a car — or unsecured. When you have a secured loan, the lender can seize the asset if you don’t keep up with your scheduled payments.

The table below outlines the differences between secured and unsecured loans.

| Loan Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral Required? | Yes (house, car, savings) | No |

| Interest Rates | Lower | Higher |

| Approval Difficulty | Easier with collateral | Harder without strong credit |

| Risk to Borrower | Asset loss if unpaid | Damage to credit score if unpaid |

Factors That Affect Loan Approval

When it comes to getting approved for a bank loan, many factors come into play. Below is a look at some of the most important factors:

- Credit score. Typically, borrowers with higher credit scores enjoy lower interest rates and better approval chances.

- Income and employment. Most lenders prefer to work with borrowers who have stable incomes to support loan repayment.

- Debt-to-income ratio (DTI). Your DTI reflects how much of your monthly income is consumed by your current debts. In general, a lower DTI indicates more bandwidth to repay the loan.

- Collateral. Depending on the loan, you may or may not need to provide collateral. Typically, providing collateral leads to better approval odds.

To qualify for a loan, you must meet basic eligibility requirements. The bank will look at your personal credit history, credit score, the amount of debt you currently owe and your payment history. Banks will consider how much you currently make compared to your debt load with your new loan. If you owe too much money, you might not be approved for a new loan.

Tips for Getting Approved for a Bank Loan

If you want to get approved for a bank loan, use the following tips to improve your chances.

- Check your credit. Before you apply for a loan, check your credit to see where you stand. Depending on your situation, you might find a great credit score, which could make getting a loan easier.

- Improve your credit. If your credit score isn’t where you want it to be, consider working on your credit before applying for a bank loan. For example, you might commit to making on-time payments and paying down debt for the next year to potentially improve your credit score.

- Lower your DTI ratio. Make an effort to lower your DTI by paying off some of your existing debts. When possible, start by paying down your high-interest debt, like credit card balances, ahead of schedule.

- Gather your documents ahead of time. You’ll need lots of paperwork to get approved for a loan. Making the effort to gather your documents, like proof of income and your Social Security number, ahead of time can speed up the process.

Is a Bank Loan Right for You?

Whether or not a bank loan is right for you depends on your situation. Before applying to a bank loan, do your research and assess your budget to confirm you can support the ongoing payment. If you can afford the payments and the loan fits into your long-term financial goals, then a bank loan might be right for you. If you aren’t sure how you’d swing the monthly payment, then a bank loan might not be right for you.

Miriam Caldwell contributed to the reporting of this article.