Survey: Debt Is the No. 1 Financial Roadblock of 2020

Written by

Joel Anderson

Written by

Joel Anderson

Edited by

River Jean-Noel

Edited by

River Jean-Noel

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

Many Americans are well aware of the budgeting strategies they should be following to keep their finances in good shape, but major financial roadblocks prevent them from achieving their savings goals. While many of these roadblocks grow out of irresponsible behaviors, plenty of others result from either unavoidable circumstances or a few careless mistakes. After all, even a few months of poor credit card usage can turn into a decade-plus of paying compound interest — potentially crushing your ability to reach financial milestones for the foreseeable future.

“Debt is a challenge for working families because so many of them are living within a couple hundred dollars of what they make each month,” said Michael Grieg, owner of the personal finance blog NinjaBudgeter. “When you have debt, you’re using that money that could be saved or invested to service the debt.”

To find out the biggest financial roadblocks for Americans in 2020, GOBankingRates surveyed nearly 900 people who are currently carrying household debt and asked them about their goals, priorities, obstacles and game plan for tackling debt. The results painted a picture of how debt can ultimately become a massive barrier to Americans who are striving to secure the life that they want.

GOBankingRates’ survey covers the following topics:

- Key Findings

- Debt Will Stop 58% of American From Reaching Their 2020 Goals

- Debt Has Caused Stress, Sleepless Nights for Many Americans

- Saving For Retirement Is the Top Priority Once They’re Debt-Free

- How To Eliminate Your Debt in 2020

Key Findings

Here are some of the most notable takeaways from the survey:

- Nearly 60% of Americans said that some form of debt would keep them from achieving their financial goals in 2020. In particular, 22% of respondents cited credit card debt as an obstacle, and 18% brought forth their student loan debt. Looking back, household debt has prevented 28% of Americans from reaching their 2019 goals.

- About 58% of respondents said they would need to make more money to get out of debt faster. In comparison, only 35% said they need to follow a budget and control their spending.

- Approximately 1 in 4 said their debt left them in a state of constant stress, and almost 1 in 5 described dealing with several sleepless nights as a result of the money they owe. In fact, 12% of respondents have been brought to tears over the amount of debt that they have. To put things into perspective, the average total household debt for each American is a staggering $46,330.53.

- Eliminating debt was a goal for almost half of those surveyed. Americans also said they wanted to raise their credit score and stop living paycheck to paycheck, with 29% and 28% of respondents choosing these options, respectively. To do this and break the cycle of debt, they may need to learn the true cost of borrowing money.

Debt Will Stop 58% of Americans From Reaching Their 2020 Goals

Over half of all survey respondents cited their credit card debt, student loans, mortgage or auto loans as a key roadblock to accomplishing everything they want to achieve in 2020. That’s not surprising, given how much total household debt Americans claimed to have. The average debt across all groups was a whopping $46,330.53 — a figure that can easily leave some families under the shadow of financial instability.

| Americans’ Biggest Roadblocks To Accomplishing Their Goals in 2020 | |

| Roadblocks | Response Rate |

| My low salary/income | 33.71% |

| I don’t anticipate having any roadblocks in 2020 | 29.76% |

| My credit card debt | 22.10% |

| My student loan debt | 18.26% |

| My housing costs (including rent) | 18.26% |

| My family expenses (i.e., child care, college) | 11.72% |

| My mortgage | 10.26% |

| My auto loan debt | 7.33% |

| A major life event (e.g., wedding, divorce, having a baby) | 6.43% |

| Other | 3.38% |

“Debt is such a big problem because amortized interest is the exact opposite of compound interest we can earn in an investment,” said Garrett Konrad, a partner and investment advisor at IFC and Insurance Marketing Inc. “If you think about compound interest, it is fairly underwhelming at first, and the longer time period you have to grow assets, the more meaningful and overwhelming it becomes. Amortized interest and interest we pay on debt is the exact opposite in that we feel it is benign until it becomes an out-of-control problem.”

Related: The Average Student Loan Debt in Every State

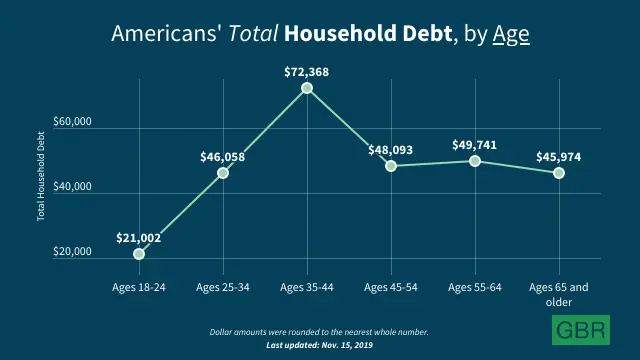

Digging a little deeper into the demographic breakdown also resulted in some fascinating findings. Debt appeared to peak at an average of $72,367.52 between ages 35-44, which is understandable — financial obligations like mortgages, student loans and child care expenses may start overlapping at this time of life. However, debt for other demographics ages 25 and older consistently averaged between $45,000-$50,000, which means that the $70,000-plus balance for the 35-44 age group is clearly an outlier. Additionally, it’s troubling that reported debt only declines slightly for respondents ages 65 and older. Americans could be entering retirement while saddled with concerning levels of debt.

On average, female respondents had approximately $4,000 more in debt than their male counterparts. They were also more likely to cite a low salary as a major roadblock — 38% of women versus 30% of men chose this option — which might indicate that it’s more difficult for women to pay down their debt and avoid adding to it in the first place. Supporting this finding, only 26% of female respondents said they don’t anticipate facing any roadblocks in 2020, compared with 33% of male respondents.

However, although some form of debt surfaced repeatedly as a roadblock, the two answer choices that received the highest number of responses aren’t necessarily related to debt. One-third of respondents said their low income would prevent them from reaching their goals in 2020, and about 30% said they aren’t expecting to encounter any roadblocks, showing that a large segment of those polled is either in great financial shape or just wildly optimistic.

Don’t Miss: Best Balance Transfer Credit Cards of 2019

They Want To Save Money, Improve Their Credit and More

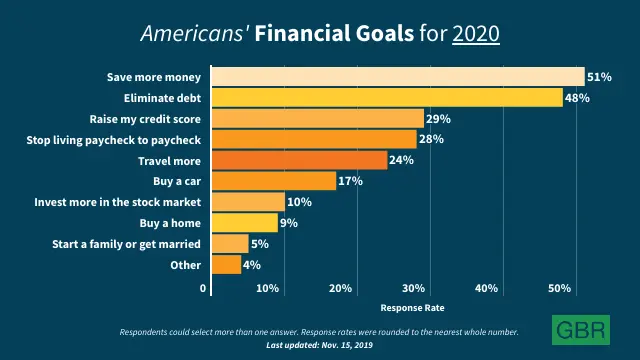

If Americans actually achieved their financial goals for 2020, they would directly address their issues with debt and set themselves up for more ambitious goals in the future. Over half of all survey respondents said their goal was to save more money, which is one of the clearest paths to eliminating — and preventing — debt. Having an emergency fund stashed in a high-yield savings account can stop an unexpected medical bill or layoff from evolving into serious levels of debt.

Of course, eliminating that debt in itself was another major goal for survey respondents. Nearly half of those surveyed said that getting rid of debt is among their financial goals for 2020. Beyond that, over 1 in 4 Americans wanted to raise their credit scores and stop living paycheck to paycheck — both of which are closely related to debt as a financial roadblock.

However, there are plenty of reasons to worry about the impact of debt on Americans’ lives. Major financial goals — like investing more in the stock market, buying a home or starting a family — all appeared to be less important to many survey respondents than basics like saving more money and paying off debt. Essentially, consumer debt might be causing significant delays in achieving certain life milestones.

“If someone wants to borrow from a bank to buy a house, other debt might be an impediment,” said Megan Gorman, a managing partner at Chequers Financial Management. “As a result, the traditional American avenue to building up one’s net worth gets blocked.”

Debt Has Caused Stress, Sleepless Nights for Many Americans

Aside from putting financial milestones on hold, debt can have even broader implications, like causing constant stress and creating problems in personal relationships. While it’s fortunate that about 40% of survey respondents haven’t dealt with these issues, other Americans have seen their debt develop into crises beyond their financial lives. Over 1 in 4 respondents said they’re constantly stressed over their debt, and 18% said they’ve spent several sleepless nights because of it — both of which can contribute to a range of worrisome health issues.

| Impact of Debt on Americans’ Personal Lives | |

| Statement | Response Rate |

| My debt has prevented me from achieving my goals | 27.73% |

| I’m constantly stressed over debt | 26.72% |

| My debt has caused me to have several sleepless nights | 17.93% |

| My debt has prevented me from getting a loan | 13.98% |

| My debt has prevented me from getting a good credit card | 13.87% |

| I have cried over how much debt I have | 12.06% |

| My debt has caused issues in my personal relationships | 10.94% |

| None of the above | 43.18% |

| Other | 2.25% |

However, the data broken down by age demographic shows that there might be light at the end of the tunnel. Stress over debt peaks between ages 35-54, which largely corresponds to the period of life when respondents reported having the most debt. While debt doesn’t necessarily decline as you pass the age of 55, based on the survey results, stress levels appear to do so. About 32% of 35- to 44-year-olds and 33% of 45- to 54-year-olds reported constant stress over their debt in 2019, compared with 27% of 55- to 64-year-olds and only 22% of respondents aged 65 and older — the lowest stress level among all age groups.

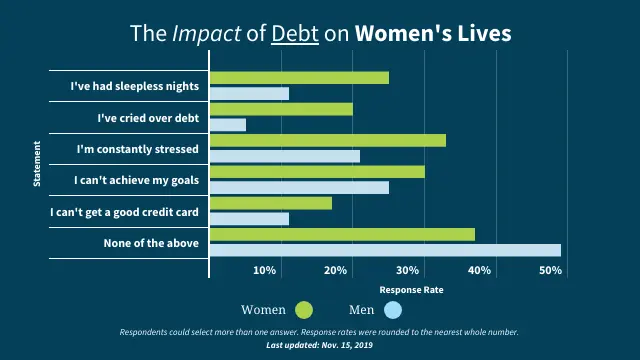

In terms of the impact of debt on their lives, female respondents expressed a lot more worry about their finances than male respondents did. About 25% of women versus 11% of men said they faced several sleepless nights in 2019 due to their debt. Female respondents were significantly more likely than male respondents to have cried over how much debt they have, at 20% and 5%, respectively. And, more women were constantly stressed over their debt compared to men — a difference of 12 percentage points. It’s important to note that female survey respondents also reported making less money and carrying more debt than male respondents, which means they might have more reasons to stress out and lose sleep.

Read More: Many Americans Would Sacrifice Having a Family To Avoid Credit Card Debt

Saving For Retirement Is the Top Priority Once They’re Debt-Free

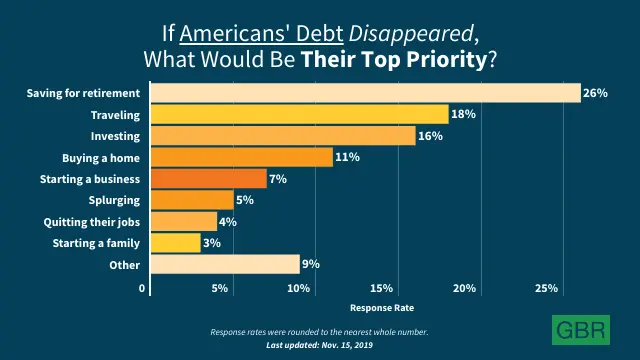

So, what would Americans do if they were free from debt? On the whole, they seem committed to making long-term financial plans. About 54% of survey respondents said they would either save more for retirement, invest more money or buy a home, all of which are important goals — which once again illustrates how debt can be a major roadblock to building the sort of responsible financial life that Americans want.

Interestingly, traveling more is the No. 1 thing that 18% of respondents said they would do if they could get rid of their debt, and it was the second-most popular answer choice. This statistic could indicate that debt is causing people to forgo vacation time — and self-care — that would otherwise help alleviate the negative health effects of financial stress. At the same time, it’s wiser in the long term to invest any extra money or save it into an emergency fund or retirement account, rather than spend the money on a vacation.

Find Out: Best Cities To Live In If You Want To Pay Off Your Student Loans Quickly

In the event that their debt was wiped out, Americans ages 55-64 were the most likely to save more for retirement, with 37% of respondents in this age group choosing to tackle their nest egg. This trend makes sense, since retirement is fast approaching for 55- to 64-year-olds. It’s also interesting to note that 18- to 24-year-olds — the youngest age group in the survey — were far more likely to invest once debt was out of the equation, showing financial savvy. About 33% of respondents ages 18-24 chose investing more money as their top priority, compared with 16% of 35- to 44-year-olds, which was the next-highest response rate for this option.

| The No. 1 Thing Americans Would Do If They Could Eliminate or Reduce Their Debt | ||||

| Demographic | Answer Choice | |||

| Save More For Retirement | Invest More Money | Buy a Home | Travel More | |

| Ages 18-24 | 9.26% | 32.72% | 11.11% | 16.05% |

| Ages 25-34 | 23.21% | 15.18% | 9.82% | 17.86% |

| Ages 35-44 | 31.78% | 15.50% | 17.05% | 13.18% |

| Ages 45-54 | 31.06% | 12.42% | 14.29% | 15.53% |

| Ages 55-64 | 37.27% | 7.45% | 9.32% | 20.50% |

| Ages 65 and older | 26.54% | 14.20% | 7.41% | 24.07% |

| Men | 22.89% | 20.73% | 11.23% | 17.49% |

| Women | 30.42% | 11.56% | 11.56% | 18.63% |

In comparison, women were more likely than men to prioritize saving more for retirement, at 30% and 23%, respectively. It’s possible that women could be further behind in their retirement savings, given the gender pay gap and their higher levels of debt. Conversely, male respondents were more likely than female respondents to choose investing more money — 21% vs. 12%, respectively — which is a tried-and-true path to building wealth.

How To Eliminate Your Debt in 2020

According to GOBankingRates’ survey, 58% of Americans think that making more money is the key to getting out of debt faster. While this plan will almost certainly work, it’s not a strategy that people can reliably deploy on their own. There are definitely long-term career moves that can boost your earning power, but securing a raise in the next year can be difficult. Instead, you should consider alternative options, like refinancing your loans or creating a realistic budget — and sticking to it.

“In order to get out of debt, you need to be actively managing it. Whether you’ve got student loans, credit card, or mortgage debt, it’s hard to make a dent in your loan principal if too much of your monthly payment is going toward interest charges,” said Robert Humann, general manager of student and personal loans at Credible. “All types of debt can be refinanced — you can often pay off credit card debt with a personal loan that’s got a lower interest rate, for example. The key to getting lower rates when refinancing is to first work on improving your credit score, and then get rates from multiple lenders.”

Additionally, following a budget and controlling your spending — the second-most common response to GOBankingRates’ question about ways to eliminate debt — hits on a basic approach that people of any profession or income level can rely on. There’s nothing else that can universally benefit someone’s financial situation in the same way.

“In terms of managing debt, it’s all about the basics,” Gorman said. “It’s about building a budget and sticking to it. There isn’t any magic wand that can change this. That’s why it’s so hard for Americans to get out of debt.”

Everything You Need To Know About Budgeting: How To Create a Budget You Can Live With

While adhering your spending to a budget might seem simple, there’s a reason why so many Americans are deeply in debt — budgeting can be much more difficult in practice. However, the discipline pays off in a bright financial future, free of debt-related stress.

“It will take some short-term sacrifice, but it is going to give you the rest of your lifetime to be in a stronger financial position if you do it now,” Konrad said. “Cancel dinners out, get creative with date night on a budget, put your athletic club membership you use twice a month on hold, and really try to just hammer your debt with cash flow.”

More From GOBankingRates

- Here Are 30 Ways To Retire Earlier

- Are High-Yield Savings Accounts Worth It? Here’s Everything You Need To Know

- Questions To Ask Before Taking Out a Personal Loan

- Best TD Bank Promotions

Grace Lin contributed to the reporting for this article.

Last updated: Nov. 19, 2019

Methodology: GOBankingRates surveyed 887 Americans ages 18 and older from across the country between Oct. 23, 2019, and Nov. 7, 2019, asking six different questions: (1) What are your financial goals for 2020? Select all that apply; (2) Do you anticipate any of the following will prevent you from accomplishing your goals in 2020? Select all that apply; (3) Of the following, what do you think you need in order to get out of debt faster? Select all that apply; (4) What’s the No. 1 thing you would do if you could eliminate or reduce your debt? Select ONE; (5) By your best estimate, how much total household debt (mortgage, credit card, student loans, auto, medical, etc.) do you currently have? and (6) Have any of the following statements applied to you in 2019 (so far)? Select all that apply. All respondents had to pass a screener question, “Do you currently carry any sort of household debt (i.e. credit card debt, mortgage debt, student loan debt, auto loan debt, etc.)?” with the answer of “yes.” GOBankingRates used Survata’s survey platform to conduct the poll. Respondents were reached across the Survata publisher network, where they take a survey to unlock premium content, like articles and e-books. Respondents received no cash compensation for their participation. More information on Survata’s methodology can be found at survata.com/methodology.