Survey: Why ‘Setting and Forgetting’ Is Hurting Americans’ Retirement

Written by

Grace Lin

Written by

Grace Lin

Edited by

River Jean-Noel

Edited by

River Jean-Noel

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

While chasing the market isn’t advisable, neither is “setting and forgetting” your retirement plan, as it turns out. If your involvement ends at automatic payroll deductions to your 401(k) or individual retirement account, you might not be putting your hard-earned nest egg to work in the right ways.

“Over time, your financial situation and your ultimate goals can change, sometimes dramatically,” said Judith Corprew, executive vice president and chief compliance and risk officer of Patriot Bank, N.A. “For this reason, it makes sense to reevaluate your retirement plan regularly.”

To find out exactly how Americans are handling their retirement savings, GOBankingRates conducted a survey of 803 respondents, asking about their retirement account balances, how often they check and rebalance those accounts, and their confidence levels toward their chosen investing approach.

Based on the survey results, GOBankingRates explores the following topics:

- Key Findings

- People Who Set and Forget Their Retirement Plan Contribute More

- But Their Money Might Not Actually Be Going Further

- Why You Should Pay Closer Attention To Your Retirement Savings

Learn Now: How To Open a Roth IRA

Key Findings

- About 14% of Americans set and forget their retirement savings. Of the survey respondents who employ this investment approach, 15% have less than $1,000 in their 401(k) or IRA.

- Many people had no idea how much they have saved. Roughly one-third of overall survey respondents said they didn’t know their retirement account balance. In particular, it’s concerning that 37% of Americans ages 65 and older were in the dark about their savings.

- Women are contributing far less to their retirement savings than men, and twice as many female respondents couldn’t provide an estimate of their account balance. Women contribute an average of $1,331 annually, whereas men add $2,633 per year, on average, to their retirement accounts — a difference of more than $1,300.

- Keep an eye on your investments as life progresses, checking to see if your retirement savings accounts continue to align with your goals and other financial considerations. It helps if your investments are managed by the best 401(k) companies or top IRA providers.

People Who Set and Forget Their Retirement Plan Contribute More

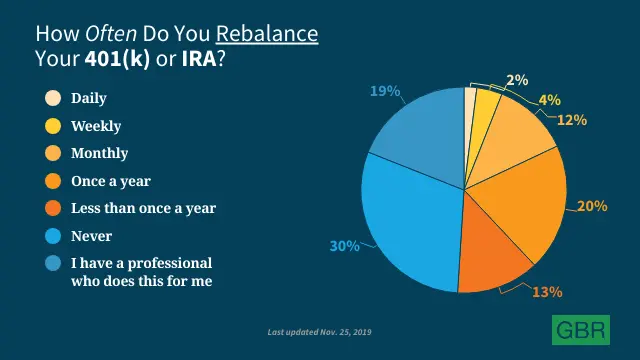

While 42% of Americans who have a 401(k) or IRA said they look up the balance every month — it was the most popular response among overall survey respondents — 14% said they never check on their retirement savings account. Even fewer people rebalance or reallocate their retirement plan on a regular basis. About 30% have never taken such steps, and 19% rely on a professional to do it for them.

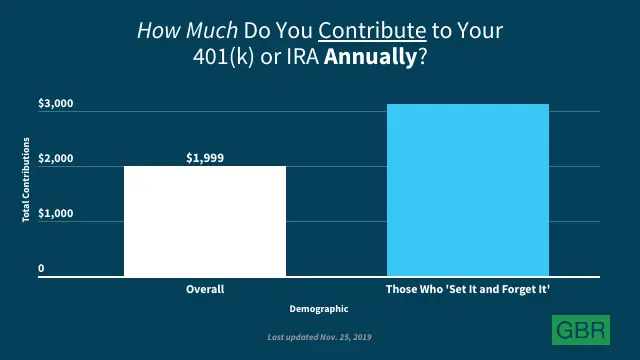

On average, Americans contribute $1,999 per year to their 401(k) or IRA. However, people who said they tend to set and forget their retirement plan end up contributing $1,131 more, for an average annual total of $3,130. Roughly half of these individuals check the balance in their retirement accounts once a year or less.

Despite their regular contributions, 12% of overall survey respondents said they’re not sure if their 401(k) or IRA is actually doing well. About 6% think they need professional help to grow their retirement savings and wish they had more help with choosing their initial investments.

| How Much Americans Contribute To Their Retirement Savings Every Year | |

| Demographic | Dollar Amount |

| Ages 18-24 | $2,107.59 |

| Ages 25-34 | $1,758.88 |

| Ages 35-44 | $2,250.12 |

| Ages 45-54 | $2,739.19 |

| Ages 55-64 | $2,333.76 |

| Ages 65 and older | $784.32 |

| Female | $1,330.62 |

| Male | $2,633.25 |

Women contribute far less to their 401(k) or IRA than men do — in fact, they’re saving roughly half as much. However, it’s interesting to note that female respondents were also more likely to have a professional who rebalances or reallocates their retirement plan. About 22% of women versus 16% of men have gotten professional help with their investments.

Check Out: 10 Best Retirement Plans

But Their Money Might Not Actually Be Going Further

It’s reasonable to expect higher returns when you contribute more of your paycheck to your retirement plan — but that might not always be the case. Results will vary depending on the investments that you select.

“You may have chosen the default investment option within your 401(k),” said Matt Wilson, a certified financial planner, chief investment officer and managing director at Keen Wealth Advisors. “Sometimes, the default option might be an age-based mutual fund or target retirement date fund. This fund may not be appropriate for you given your specific goals and appetite for risk. Other times, the default option is a cash-like investment such as a money market fund. It is highly unlikely this investment will generate the returns needed to fund someone’s retirement goals.”

| How Often Americans Rebalance and/or Reallocate Their Retirement Savings Plan | ||||

| Demographic | Answer Choice | |||

| Never | Annually | Monthly | A Professional Does This For Me | |

| Ages 18-24 | 26.67% | 22.86% | 18.1% | 16.19% |

| Ages 25-34 | 36.36% | 21.21% | 12.12% | 12.12% |

| Ages 35-44 | 36.26% | 16.48% | 9.89% | 12.09% |

| Ages 45-54 | 35.08% | 15.71% | 10.47% | 21.99% |

| Ages 55-64 | 29.17% | 23.96% | 13.02% | 17.19% |

| Ages 65 and older | 25.13% | 19.37% | 11.52% | 22.51% |

| Female | 31.46% | 19.69% | 11% | 21.74% |

| Male | 29.37% | 19.9% | 13.59% | 15.78% |

Alarmingly, over one-third of respondents ages 25-54 said they have never rebalanced or reallocated their retirement accounts. It’s particularly concerning because people undergo many life changes during this long period of their lives, from buying their first home to having children — which means their financial goals and risk tolerance may shift considerably as well. Even worse, 29% of respondents ages 55-64, who are on the cusp of retirement, said they never rebalance or reallocate their investments.

“Even if your situation and goals remain stable, it’s still useful to think about your savings regularly,” Corprew said. “Financial advisors often recommend that individuals focus on higher-risk, higher return investments at the early stages of their career, in an effort to build wealth. But as you approach retirement, these advisors typically suggest a safety-first approach focused on maintaining the savings you already have.”

About 15% Have Less Than $1,000 in Their Retirement Accounts

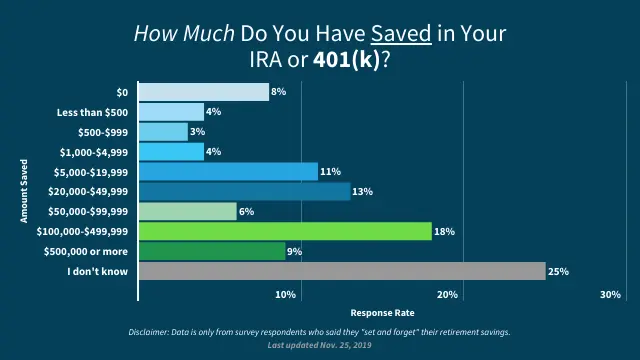

The habit of not rebalancing or reallocating your retirement plan can reflect in your account balance over time. Americans who set and forget their 401(k) or IRA were just as likely as overall survey respondents to have saved less than $1,000 for retirement — even though they contribute significantly more. About 15% of both groups revealed that they have minimal retirement savings.

“People who set and forget the automatic savings to their retirement accounts, specifically 401(k)s and IRAs, commonly make the mistake of not adjusting their dollar amount per paycheck when they receive pay increases,” said Michael Foguth, president and founder of Foguth Financial Group. “As you move up with an organization, your pay will likely increase. This in turn should increase contributions to your retirement accounts. For example, when you hired in, $100 per paycheck may have been what you could afford at the time, but 10 years later, you should not still be contributing $100 per paycheck.”

At the same time, overall survey respondents were less likely than people who set and forget their retirement plan to have $100,000 or more saved — at 20% and 26%, respectively — so this strategy can seemingly go both ways. About 30% of overall respondents had no clue how much they have saved in their 401(k) or IRA.

| How Much Americans Have Saved in Their 401(k) or IRA Right Now | ||

| Demographic | Answer Choice | |

| Less Than $1,000 | I don’t know | |

| Ages 18-24 | 27.62% | 19.05% |

| Ages 25-34 | 24.24% | 30.3% |

| Ages 35-44 | 19.78% | 32.97% |

| Ages 45-54 | 12.56% | 35.08% |

| Ages 55-64 | 8.33% | 22.4% |

| Ages 65 and older | 12.57% | 36.65% |

| Female | 13.8% | 40.41% |

| Male | 15.78% | 19.9% |

About 37% of Americans ages 65 and older don’t know how much they have currently saved in their 401(k) or IRA, which was the highest response rate for this answer choice — and that doesn’t bode well for their retirement. These individuals need to keep track of how much they’re withdrawing from their savings, otherwise their retirement funds could dry up faster than expected.

Additionally, women were far more likely than men to fail at recalling their retirement account balance. A startling 40% of female respondents versus only 20% of male respondents couldn’t provide a ballpark estimate of how much they have stashed away in their 401(k) or IRA.

Don’t Miss: The 8 Best Roth IRA Providers With Low Fees & Great Perks

Why You Should Pay Closer Attention To Your Retirement Savings

People who set and forget their retirement savings were more likely than overall respondents to have a traditional 401(k) — at 65% and 53%, respectively — which might indicate that these Americans are sticking to their default employer-sponsored retirement plan. However, there are a few reasons why leaving your retirement savings alone can hurt you:

- Your retirement plan might not match your goals anymore. Your approach to investing may change before and after you take on student loans, buy a home or start a family. Likewise, Americans nearing retirement shouldn’t have the same investing strategy as most fresh college graduates.

- You aren’t taking advantage of market movements. “For example, when equities take a significant hit, you have an opportunity to buy cheap equities if you reallocate your account and move a portion of the bonds/fixed income within your portfolio to equities,” said Wesley Botto, a certified public accountant and financial advisor at Botto Financial.

- Your portfolio might not be diversified. “Mutual funds change their holdings periodically,” said Alina Trigub, managing partner at SAMO Financial. “So it is wise to see what each of the mutual funds contains to ensure that your portfolio is still diversified.”

- As a result, your nest egg is vulnerable to another recession. “If you own mostly equities at the start of a downturn, you’ll need to sell stocks at a loss to cover your living expenses,” said Kelly Crane, president and chief investment officer at Napa Valley Wealth Management. “With the combination of declining equity values and withdrawing principal to live on, the losses could take years to only break even. Instead, look to a mix of bonds and/or cash to cover your cash flow needs for a possible extended recession — up to three to five years.”

In order to achieve a diversified portfolio and ensure that your investments match your current risk tolerance, it’s wise to consider rebalancing or reallocating your retirement plan on a regular basis — even if you’d prefer to set and forget it.

“A general rule of thumb is to check up on it every quarter or so,” Trigub said.

More From GOBankingRates

- 4 Best 401(k) Companies

- IRA Contribution Limits

- Top PNC Bank Promotions

- Cashier’s Check vs. Money Order: Here’s the Difference

Last updated: Nov. 26, 2019

Methodology: GOBankingRates surveyed 803 Americans ages 18 and older from across the country between Nov. 1, 2019, and Nov. 18, 2019, asking six different questions: (1) Which of the following retirement accounts do you currently have? Select all that apply; (2) How often do you check the balance in your 401(k) and/or IRA? (3) How often do you rebalance and/or reallocate your 401(k) and/or IRA? (4) How much do you contribute to your IRA and/or 401(k) annually? (5) How much do you have saved in your IRA and/or 401(k) currently? and (6) Do any of the following statements regarding your retirement account(s) and retirement savings apply to you? Select all that apply. All respondents had to pass a screener question of “Do you have any of the following types of retirement accounts? Select all that apply” with the answer of “Some Type of IRA” OR “Some Type of 401(k).” This survey was commissioned by ConsumerTrack Inc. and conducted by Survata, an independent research firm in San Francisco. Respondents were reached across the Survata publisher network, where they take a survey to unlock premium content, like articles and e-books. Respondents received no cash compensation for their participation. More information on Survata’s methodology can be found at survata.com/methodology.

Is Leaving You Behind While the Wealthy Double Their Nest Egg")

Rule Taking Effect This Year May Affect Savers")