How Much Student Loan Debt Can You Afford?

Written by

Heather Taylor

Written by

Heather Taylor

Edited by

Mark Shrayber

Edited by

Mark Shrayber

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

Before they enroll in their dream university, many students will likely need to put together a plan for how they will fund their education. Part of this plan may rely on taking out a student loan and if so, how much they can afford to take out in student loan debt.

Read More:

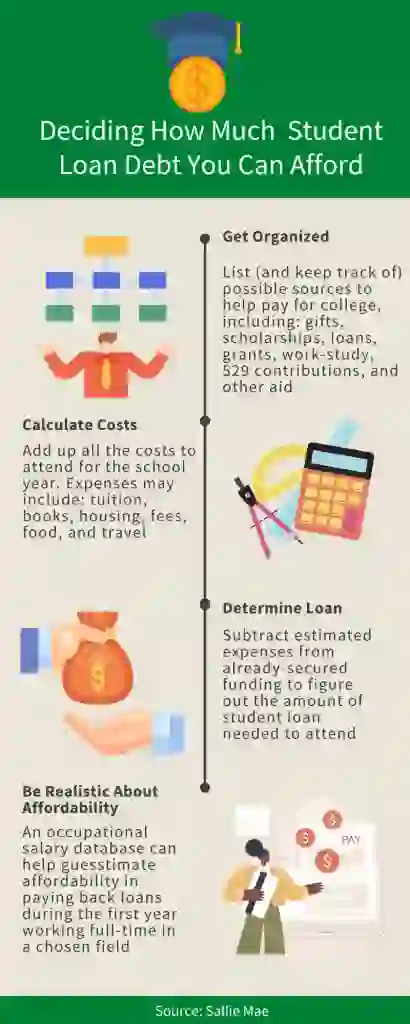

In the GOBankingRates infographic below, you’ll find steps that can help you figure out how much to take out in student loans. Let’s review these steps to see how much student debt borrowers can afford.

Get Organized and Complete the FAFSA Form

Before signing loan documents or looking into scholarships, you need to know what your financial aid eligibility looks like. The first step prospective students graduating from high school should take is completing the FAFSA form. This form will help your desired university determine your financial aid eligibility by reviewing parent and student income and assets.

Cecil Staton — CFP, CSLP, president and wealth advisor at Arch Financial Planning — said a student’s next step after completing the FAFSA form is to determine your Expected Family Contribution (EFC). From there, prospective students can consider the Cost of Attendance (COA), which is provided by most schools.

Calculate Attendance Costs

Here’s how attendance costs break down. Staton said take the COA minus the EFC to equal financial need or need-based aid. For example, if the COA for a university is $50k and the EFC is $20k, a student would need $30k of need-based aid.

In addition to tuition and fees, other costs that may be calculated include living expenses (room and board), books and supplies, transportation, equipment (usually in the form of a personal computer), costs related to a disability, an allowance for child care or other dependent care and reasonable costs for eligible study-abroad programs.

Take Our Poll: Do You Think AI Will Replace Your Job?

Research and Apply for Financial Aid Opportunities

Paying for a college education can be done with the help of scholarships, grants and more financial aid opportunities if a student is willing, organized and determined to get them.

James Lewis, president of the National Society of High School Scholars (NSHSS), recommends starting research early and applying often, making sure to identify all possible options. Ideally, students should focus their efforts on programs that are a good fit for their skills, background and interests. You can tap into funding opportunities through local community resources, religious organizations, employer programs, advocacy groups, institutional grants and national scholarship programs.

As you find relevant funding opportunities, track these sources along with their open and close dates for application deadlines.

“Open and close dates for scholarships vary greatly. Students should make applying for scholarships part of their year-round routine to maximize the potential for earning those dollars when they need them,” said Lewis. “They should also look to earn scholarships during junior and senior year of high school that can be deferred for use freshman year.”

Determine Loan

Can the prospective student’s desired school assist with the cost of their need-based aid? In addition to scholarships and grants, some universities may provide additional tuition assistance through endowments, merit-based scholarships and by pursuing work-study programs.

If none of these are offered or the student still has leftover calculated need-based aid, Staton said you’re likely looking at student loans to fund the difference. While private loans are an option, Staton recommends taking out federal loans, including Direct Subsidized Loans and Direct Unsubsidized Loans, to fund your college education.

“Direct Subsidized Loans are federal loans taken out by the student that subsidize interest accrual while in school,” said Staton. “Direct Unsubsidized Loans are also federal loans taken out by the student but don’t carry the same favorable interest subsidies.”

Additionally, parents may be able to assist students in taking out loans in the form of Federal PLUS Loan.

Be Realistic About Affordability

Jay W. Rishel, CFP at Overman Capital Management, recommends not taking out student loan debt that equals more than 1.5-2 times your expected first-year salary. A helpful benchmark is to start with an expected first-year salary within your anticipated profession and work back from there.

Students who do graduate with student loans are usually aware that their loans will be with them for some time to come. However, there are several strategies — like consolidating or refinancing loans, utilizing the avalanche or snowball repayment method or working with a financial advisor to determine a repayment plan — that can help you pay off your student debt as you ease into your career path.

More From GOBankingRates