How To Consolidate Debt With Bad Credit and Take Control of Your Finances

Written by

Joseph Hostetler

Written by

Joseph Hostetler

Edited by

Melanie Grafil, M.A., CHFC™

Edited by

Melanie Grafil, M.A., CHFC™

Commitment to Our Readers

GOBankingRates' editorial team is committed to bringing you unbiased reviews and information. We use data-driven methodologies to evaluate financial products and services - our reviews and ratings are not influenced by advertisers. You can read more about our editorial guidelines and our products and services review methodology.

20 Years

Helping You Live Richer

Reviewed

by Experts

Trusted by

Millions of Readers

If you’re wondering how to get out of debt with bad credit — know that the options are rather limited. Why’s that? To get a loan, a lender must trust that you’ll pay back the money you borrow — and a low credit score indicates that you’re a risky borrower.

For this reason, you may need a cosigner to effectively vouch for you. Or, you may have the option of submitting collateral to reassure the bank that they won’t lose money if you default on your loan.

Work with lenders that focus on those with poor to fair credit — 669 and below, according to FICO.

How To Qualify for a Debt Consolidation Loan With Bad Credit

Before you apply for a debt consolidation loan, check to see if there’s any proactive step you can take to improve your credit score.

- Are there any errors on your credit report that you can dispute?

- Can you use a tool like Experian Boost to show lenders that you faithfully pay your monthly rent and utilities?

- Can you prove you have a stable income?

It’s understandable that some financial institutions may be reluctant to extend credit to someone without a reliable paycheck. What can you do as a solution?

Get a Cosigner

You may consider applying with a cosigner who does have stable income if this is your situation. Their income and respectable credit score may be enough to push your loan application through.

Find a Lender for Poor to Fair Credit Scores

Again, some lenders specifically tout that they’re bad credit-friendly. Stick with these folks — it doesn’t guarantee an approval, but your odds are infinitely higher than trying your hand at a bank that requires good-to-excellent credit.

Best Ways To Consolidate Debt With Bad Credit

Several lenders may be able to assist you with a debt consolidation loan. With poor credit, you can’t be too choosy; but that doesn’t mean you should neglect to compare rates. Shop around a bit to see all your available options.

| Debt Consolidation Option | Best For |

|---|---|

| A personal loan from online lender | Quick approval, flexible use |

| Credit union loan | Qore forgiving credit requirements |

| Debt management plan (DMP) | Qorking with credit counselors to combine payments |

| Balance transfer credit card | Those with fair credit and short-term payoff goals |

| Home equity loan (HELOC) | Homeowners with equity — but beware that your home could be in jeopardy if you default |

Which Lenders Offer Debt Consolidation Loans for Bad Credit?

It’s worth mentioning that, as someone with bad credit, you’ll need to make the bank understand that you’re a trustworthy person — despite what your credit score indicates. Your best bet may be with local credit unions, perhaps one that you’ve built a relationship with, to whom you can explain your new situation and flex your banking history.

If you’d rather go the direction of a bank or online lender, here are a few to consider.

| Upstart | OneMain Financial | LendingPoint | |

|---|---|---|---|

| Best for | Super low credit scores | Secured options | Fair credit |

| Lowest credit score | 300 and up | N/A | 660 |

| Loan terms | 3 or 5 years | 2 to 5 years | 2 to 6 years |

| Loan amounts | $1,000 to $50,000 | $1,500 to $20,000 | $1,000 to $36,500 |

| APR | 7.80% to 35.99% | 18.00% – 35.99% | 7.99% to 35.99% |

What if You Don’t Qualify for a Debt Consolidation Loan?

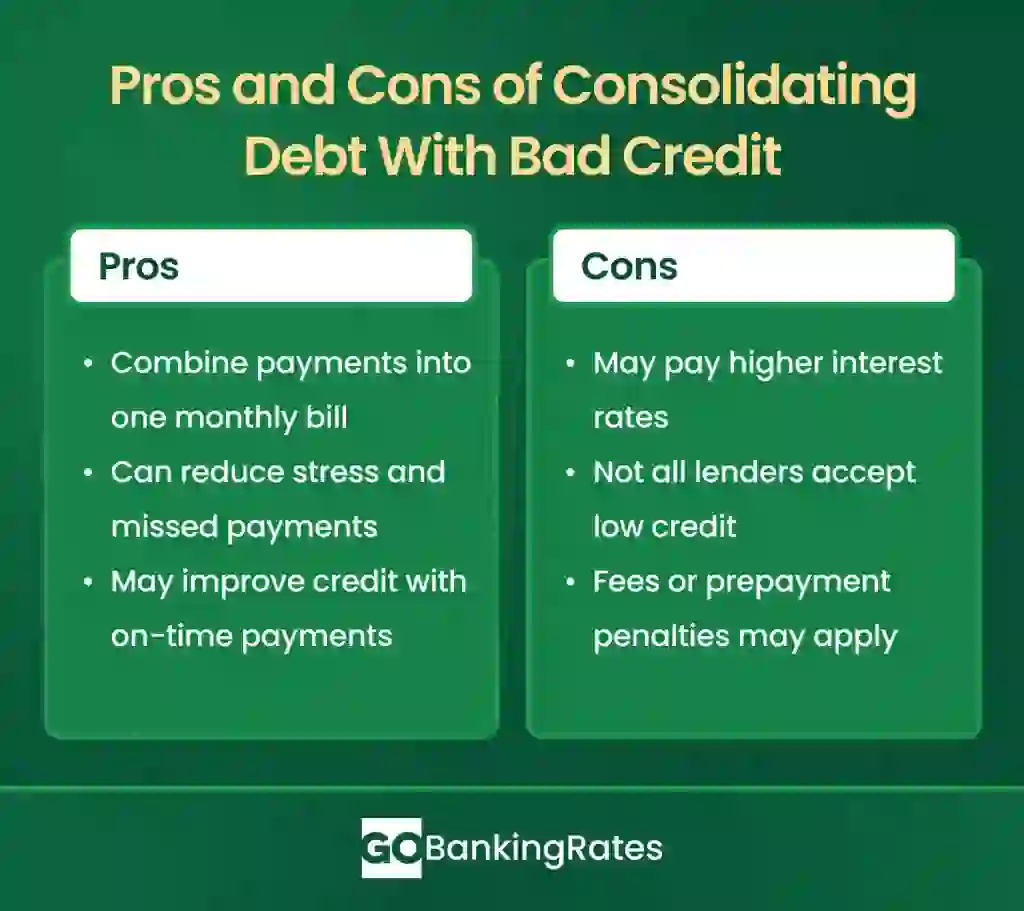

If you can’t seem to catch a break or find a cosigner to back your application, all’s not lost. You may be able to negotiate your debt yourself by calling your creditors. This can result in reduced payments, lowered interest rates and even forgiveness of some of your debt.

You can also work to build credit by opening a secured credit card, which requires a refundable security deposit, to show banks that you’re consistent with timely payments. If you’ve got multiple credit cards with balances, chip away at your current debt with strategies like the snowball or avalanche method.

For more extreme measures, consider working with a nonprofit credit counseling agency. They may help you start a debt management plan (DMP), aiding you in rolling all your debts into one monthly payment. However, all credit cards included in your DMP will likely be closed.

Who Should Consider a Debt Consolidation Loan With Bad Credit — and Who Shouldn’t

A debt consolidation loan might be right for you if:

- You have steady income and can handle fixed monthly payments.

- Your credit score is low but improving, and you meet a lender’s minimum, e.g., starting at 580.

- You’re paying high interest rates on credit cards or payday loans.

- You want to simplify payments into one due date each month.

- You’re planning to avoid new debt and stick to a budget moving forward.

- You’ve tried budgeting or debt payoff strategies, but they’re not working fast enough.

You may want to look at alternatives first if:

- You’re behind on current payments and struggling to cover basic expenses.

- You don’t qualify for a consolidation loan without very high interest rates.

- Your credit score is below 580 and lenders keep denying your applications.

- You’re already dealing with collections or legal notices from creditors.

- You’re unsure if you can commit to a new loan repayment plan.

- You haven’t explored nonprofit credit counseling or hardship programs yet.

Our in-house research team and on-site financial experts work together to create content that’s accurate, impartial, and up to date. We fact-check every single statistic, quote and fact using trusted primary resources to make sure the information we provide is correct. You can learn more about GOBankingRates’ processes and standards in our editorial policy.

- FICO. "Frequently Asked Questions About FICO® Scores in the U.S."

- One Main Financial. 2025. "Is it Hard to Get a Personal Loan?"

- Chase. 2024. "Can you get a mortgage without two years of work history?"

- Consumer Financial Protection Bureau (CFPB). "I’ve seen a lot of advertisements for companies that consolidate credit card debt. Are these legitimate?"

- Wells Fargo. "Comparing the snowball and the avalanche methods of paying down debt."